Amid Idalia’s landfall at a UBS-projected $9.36 billion total cost and a collapsing Florida home insurance market, a new study assesses hurricane risk across the United States as well as Florida’s housing market.

Florida and its relatively high, county-level concentrations of economically vulnerable mortgage borrowers in hurricane high-risk areas is the focus of the analysis from the Smith Enterprise Risk Consortium (SERC) at the University of Maryland’s Robert H. Smith School of Business.

“NOAA escalating its hurricane season forecast and Hurricane Idalia hammering parts of Florida this week underscores the need to understand the effects of these storms on the most vulnerable borrower segments, namely low-to-moderate income (LMI) and minority borrowers,” says Professor of the Practice, Executive-in-Residence and SERC Director Clifford Rossi, who conducted the study with Smith Master of Quantitative Finance student Harini Mantripragada.

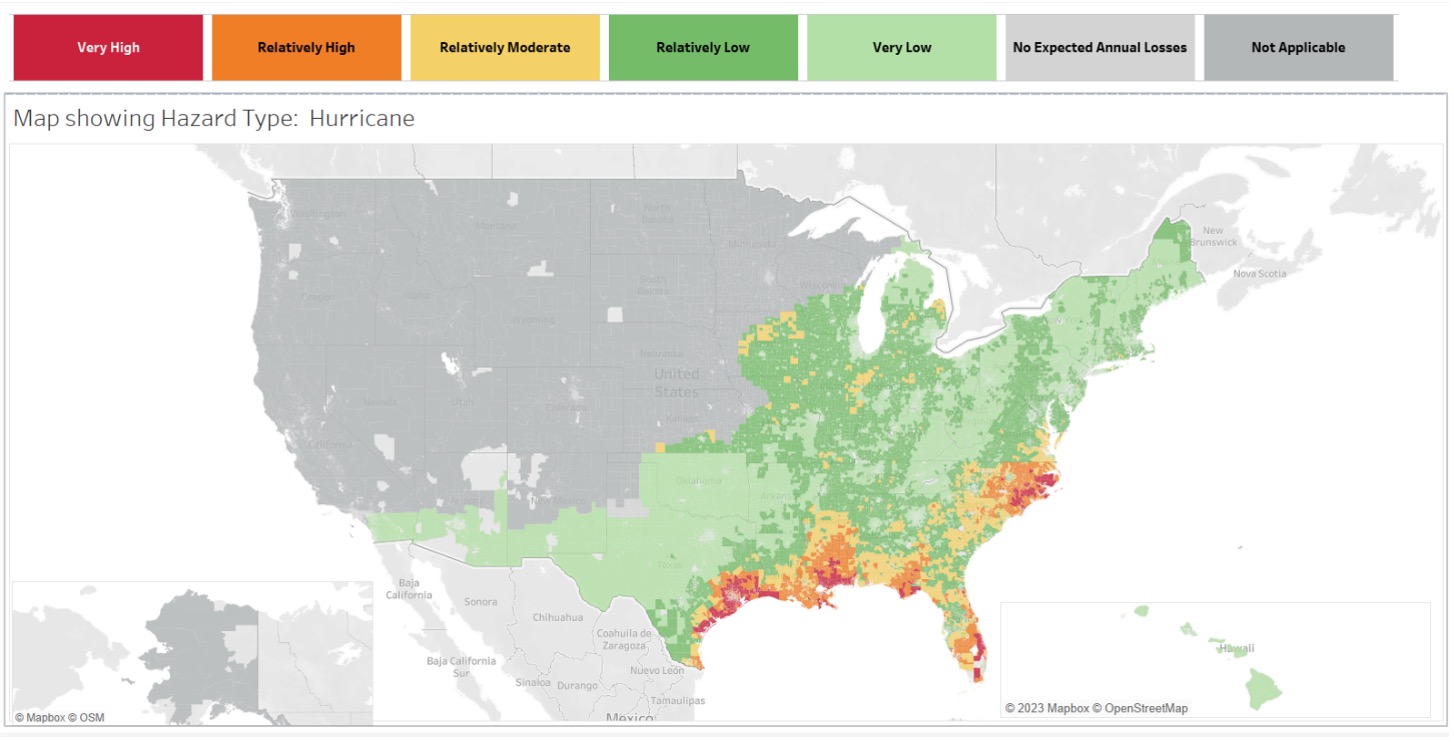

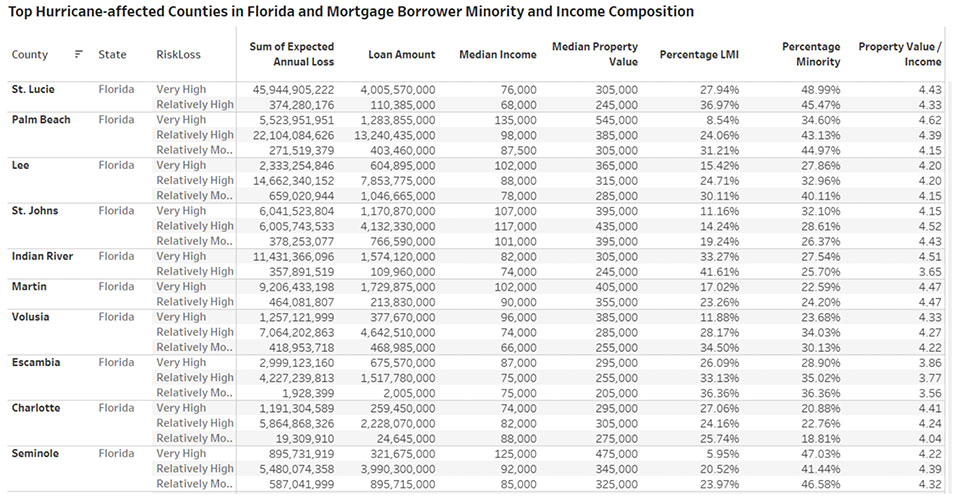

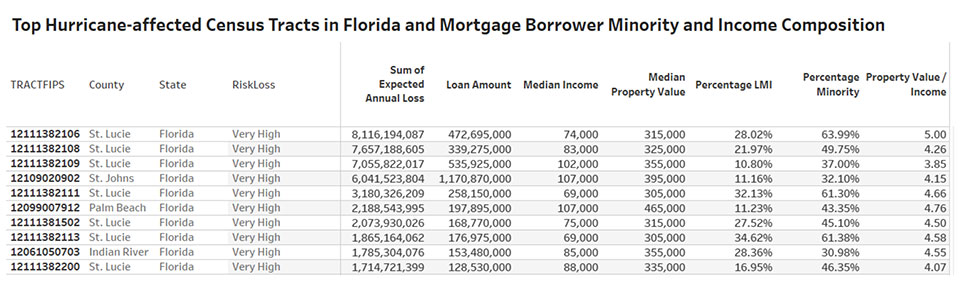

The team approached the study by taking U.S. single-family mortgages in hurricane-prone areas-- approximately 11 million loans -- originating in 2021 from the Home Mortgage Disclosure Act and merging the data with that from FEMA's National Risk Index on 18 different natural hazards -- in this case looking only at census tracts, counties and states affected by hurricanes.

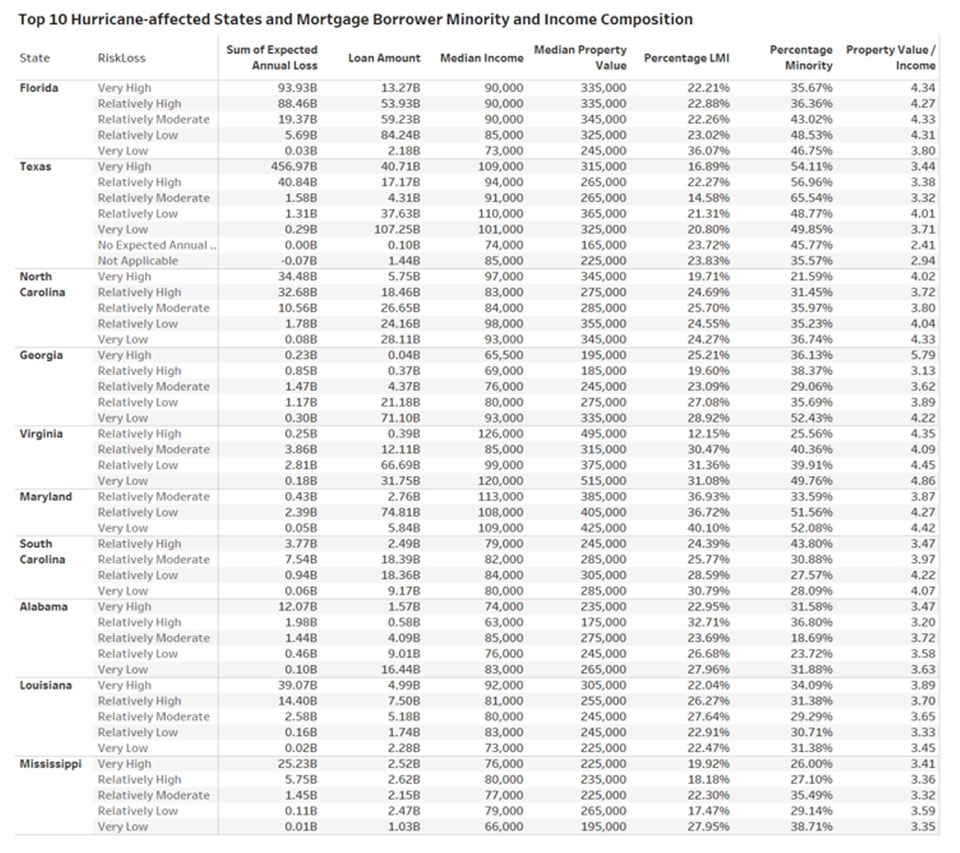

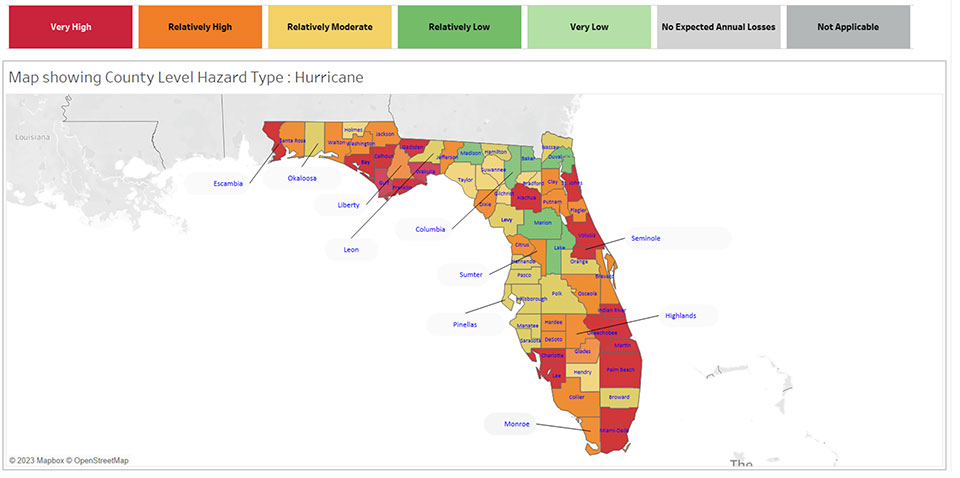

With Florida, Texas and Georgia standing out with large minority and LMI borrower segments among hurricane-affected states, they focused on Florida at the census tract level and identified several tracts across the state in high hurricane risk areas where large numbers of minority mortgage borrowers live. The team further factored in various metrics for each tract and county, such as low- and moderate-income percentages, minority percentages, median income and property values.

“Metrics such as the ratio of property value-to-income can serve as a proxy of the relative costs associated with maintaining a home to financial resources (income),” says Rossi, who has held senior risk management positions at Freddie Mac and Fannie Mae and was Managing Director and Chief Risk Officer for Citigroup’s Consumer Lending Group. “Higher ratios would be indicative of higher homeownership costs per dollar of income such that high ratios would be an indicator of financial vulnerability to a major unexpected expense, for example, a new heating system or a roof, not otherwise covered by insurance.”

Significantly, borrowers with relatively few financial resources will be more adversely affected from these storms, Rossi says. “Unexpected costs from damages such as homeowners’ insurance deductibles, and an array of post-storm out-of-pocket expenses can pose extreme financial stress on these borrowers with limited emergency savings as a buffer.”

The analysis is part of a forthcoming Mortgage Climate Risk Analyzer accessible from SERC on a subscription basis.

For more information, visit the Smith Enterprise Risk Consortium homepage.

Media Contact

Greg Muraski

Media Relations Manager

301-405-5283

301-892-0973 Mobile

gmuraski@umd.edu

Get Smith Brain Trust Delivered To Your Inbox Every Week

Business moves fast in the 21st century. Stay one step ahead with bite-sized business insights from the Smith School's world-class faculty.