Many Maryland homeowners are increasingly faced with the threat of costly home repairs from extreme weather events. With climate change, these events are becoming more frequent and more intense. And that could mean bigger problems for homeowners – particularly those who don’t have the extra cash to handle repairs.

That’s why Maryland Smith’s Clifford Rossi has developed the Homeowner Financial Vulnerability Index (HFVI), specifically categorizing the risk of weather-related damage for Maryland homeowners. The index can be used to identify regions in the state where residents are most likely to feel financial strain from getting hit with an unexpected large out-of-pocket expense, such as repairs following a big storm or flood.

Download the PDF of the research

Rossi, Professor of the Practice in finance and a risk management industry veteran, says figuring out these pockets of vulnerability is critical for tailoring targeted financial products and services to help homeowners, and for governments to determine where public investments in weather resiliency projects are most needed.

Rossi’s index combines homeowner financial vulnerability ratings with the areas of the state mostly likely to experience extreme weather events that could hit homeowners the hardest. The index incorporates Home Mortgage Disclosure Act data for every loan originated in Maryland for 2021, plus loan-level credit performance data from government-sponsored enterprises Fannie Mae and Freddie Mac. It also uses data from the Federal Emergency Management Agency (FEMA) National Risk Index that provides a rating and score at the U.S. Census tract or county level for 18 different natural hazards. FEMA’s calculations are composed of three factors: expected annual losses from 18 types of hazards; a measure of a community’s ability to deal with a natural hazard, based on things like capital and infrastructure; and a social vulnerability score.

In Maryland, the most threatening hazards are drought, tornados and coastal flooding.

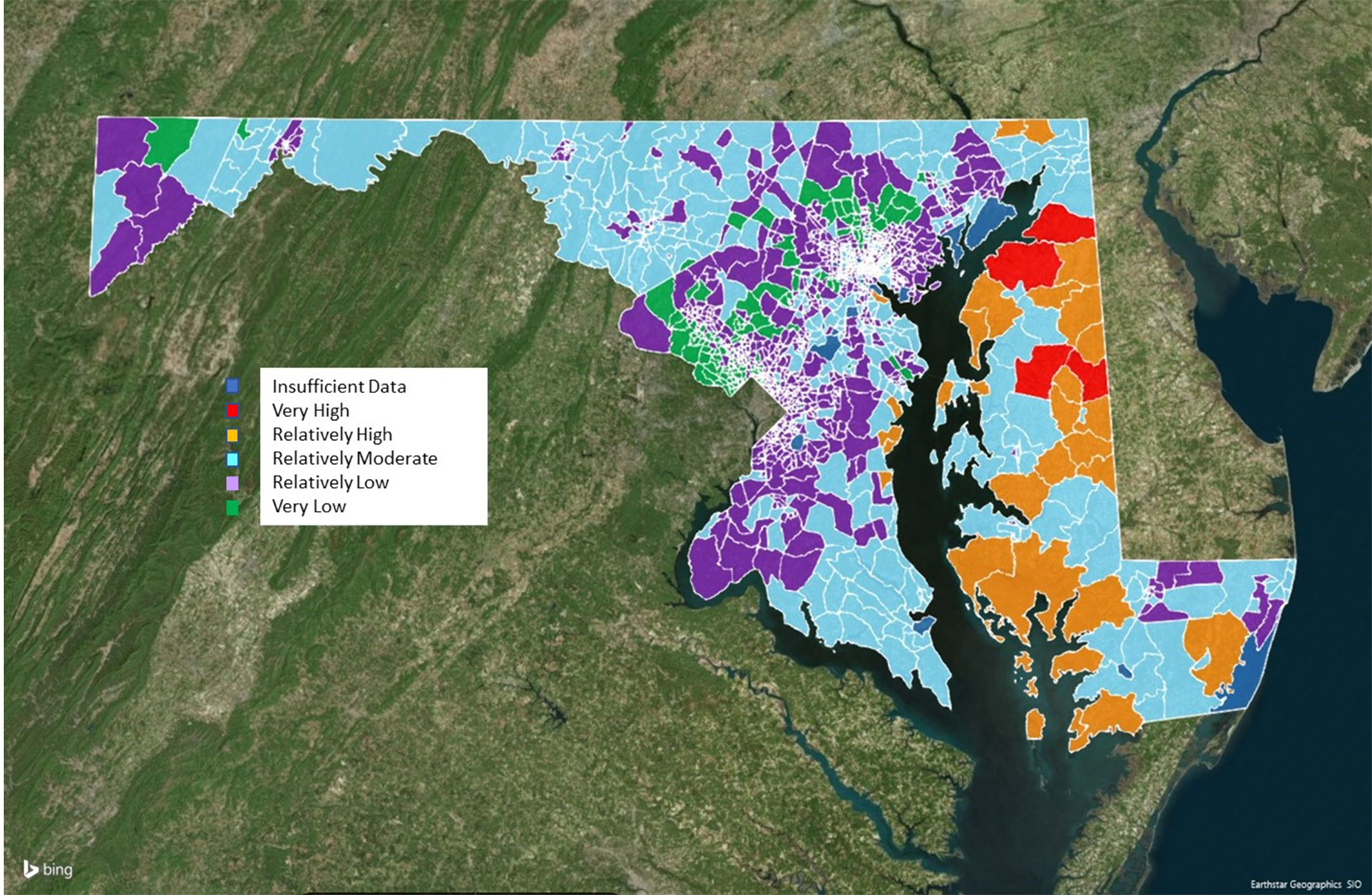

According to Rossi’s index, only four areas in Maryland are designated as having very high combined hazard risk and financial vulnerability. In addition, 30 more tracts fall into the next highest risk category. Most of these high-risk tracts are on Maryland’s Eastern Shore, and some are along the western shore of the Chesapeake Bay. “These areas are some of the least densely populated areas in the state where agriculture and fishing are major industries,” Rossi writes in the study. They also have low minority populations.

The vast majority of tracts in Maryland have relatively moderate or low risk.

“This study provides new tools for analyzing the effects of extreme weather events and homeowner financial resiliency,” says Rossi. “Identifying areas with the greatest

exposure to extreme weather and high homeowner financial vulnerability can help target public and private resources optimally.”

For example, federal, state and local funding could be used to make investments in shoreline protection or flood control measures. The findings could also help insurances and mortgage providers come up with innovative products for individual homeowners in high-risk areas.

“Current and prospective homeowners living in high hazard risk areas will need new products and services to help them understand and manage the physical and financial risks they face from extreme weather events now and in the future,” Rossi writes. “For new homeowners, having tools that help identify the physical risks of their area is critical before making a purchase.”

He says current homeowners can also benefit from his index and other tools, especially forward-looking tools that can provide them with perspectives on hazards happening not just this year but in the next decade and more in the future.

“As the frequency and severity of extreme weather events increases, today’s seemingly low-risk property might become tomorrow’s high-risk home, making the need to obtain insurance more critical,” Rossi says. “And with flood risk being just one of many potential hazards to a home over the life of a mortgage, providing homeowners with better information is imperative.”

Financial products, such as adjustable balance mortgages, could be used to incentivize homeowners to make proactive investments in projects to shore up their property to make it more resilient to weather extremes, he says. And other post-disaster financial products could be developed to provide relief for homeowners facing renovations and repairs not covered by insurance.

“Ultimately, the first step in developing these capabilities, products and programs is to identify those homeowners most in need of help,” says Rossi. “Tools such as the Homeowner Financial Vulnerability Index when combined with FEMA’s NRI data can provide the kind of information needed to better insulate homeowners from the unexpected costs of extreme weather events.”

Media Contact

Greg Muraski

Media Relations Manager

301-405-5283

301-892-0973 Mobile

gmuraski@umd.edu

Get Smith Brain Trust Delivered To Your Inbox Every Week

Business moves fast in the 21st century. Stay one step ahead with bite-sized business insights from the Smith School's world-class faculty.